Trying to time the stock market is like trying to predict the weather—sometimes you’re spot on, but more often, you’re caught in the rain. For most investors, the stress of guessing when to buy low and sell high is a losing game. That’s where dollar-cost averaging (DCA) comes in: a simple, disciplined strategy that takes the guesswork out of investing.

In March 2025, with markets still swaying from economic shifts, DCA offers a steady path to wealth. So, what is it, and how can it work for you?

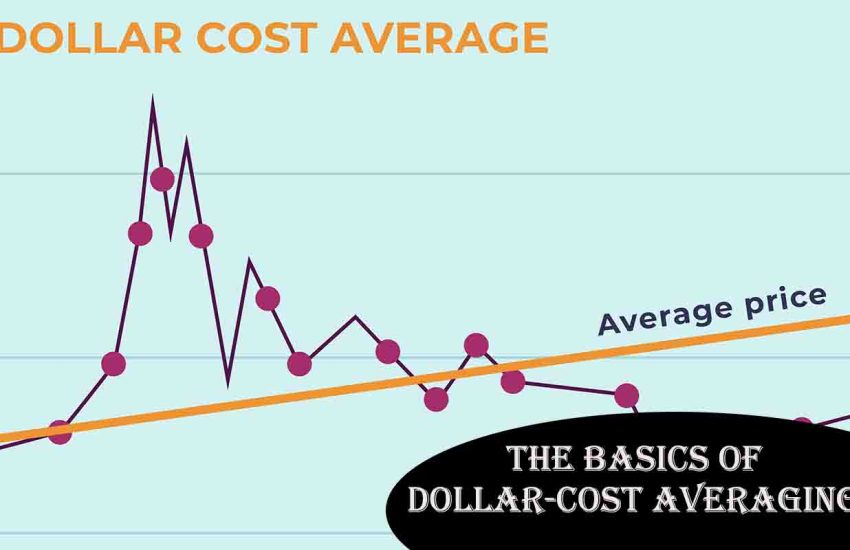

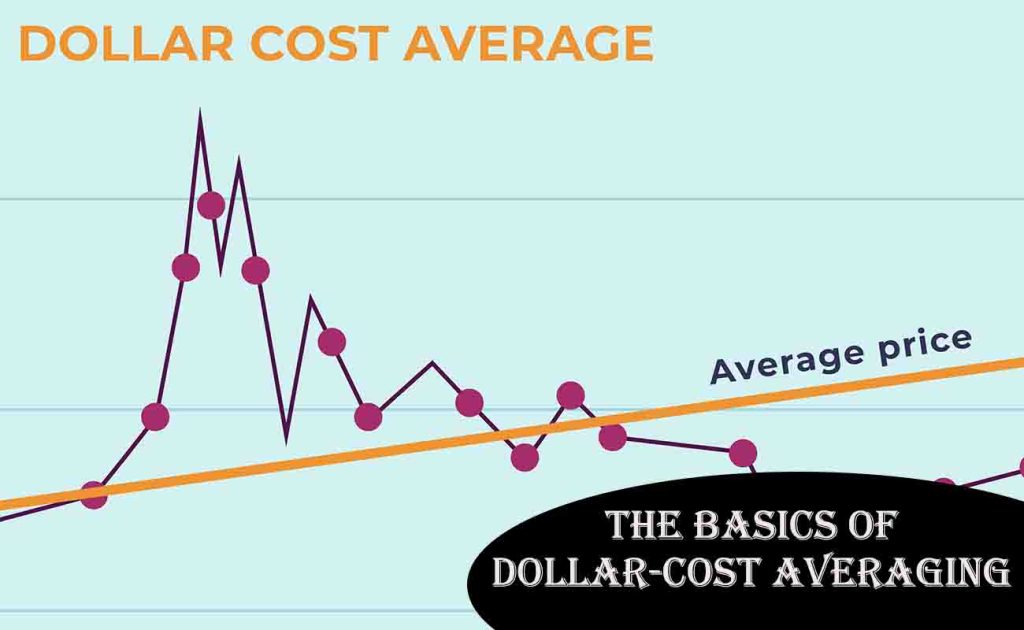

What Is Dollar-Cost Averaging?

Dollar-cost averaging means investing a fixed amount of money at regular intervals—say, $200 every month—regardless of whether the market is up, down, or sideways. Instead of dumping a lump sum into a stock or fund at one price, you spread your buys over time. When prices are high, your $200 buys fewer shares; when they’re low, it buys more. Over time, this averages out your cost per share, smoothing the ride through market bumps.

Benefits: Reducing Risk, Avoiding Emotional Decisions

DCA shines because it’s built for the real world:

- Lowers Average Cost: By buying more shares when prices dip, your overall cost per share often ends up lower than the average market price.

- Reduces Risk: You avoid the trap of investing everything at a peak, only to watch it crash.

- Curbs Emotion: No panic-selling or FOMO-buying—just steady, automatic investing.

Imagine putting $2,400 into an ETF all at once in January at $100 per share (24 shares). If the price drops to $80 by July, you’re down $480. With DCA, investing $200 monthly over a year, you’d buy at varying prices—more shares at $80, fewer at $100—ending with a lower average cost and less stress.

How to Implement DCA in Your Portfolio

Getting started is easy:

- Set a Budget: Decide what you can afford monthly—$50, $500, whatever fits.

- Choose an Investment: Index funds or ETFs (like the S&P 500) are DCA favorites for their diversification.

- Automate It: Use your brokerage or 401(k) to schedule contributions—set it and forget it.

- Stick with It: Consistency is key, even when headlines scream “market crash.”

A 25-year-old investing $200 monthly in an S&P 500 fund at a 7% average return could have over $260,000 by age 65—without ever timing a single dip.

When It Works Best

DCA thrives in volatile markets, where prices swing wildly—think 2020’s pandemic plunge or 2025’s ongoing recovery waves. It’s less ideal in a steady bull run, where a lump sum might outpace it by catching early gains. But since no one has a crystal ball, DCA’s strength is its reliability: it keeps you in the game without the gamble.

The Bottom Line

Dollar-cost averaging isn’t flashy—it won’t make you an overnight millionaire. What it does is turn investing into a habit, not a high-stakes bet. In 2025, as markets ebb and flow, DCA offers a calm, proven way to build wealth over time. Start small, stay consistent, and let the math do the work. You don’t need to outsmart the market; you just need to outlast it. Ready to take the plunge? Your future self will thank you.